Note: The information in this sample is specific to the RUN Powered by ADP® (RUN) platform only and should not be used as the official W-2. Use the detailed instructions for Form W-2. Additionally, there are no changes to the Form W-2 for tax year 2025.

Distributing W-2s to your employees each year is a critical activity. Employers must complete, file with the Social Security Administration, and furnish to employees a Form W-2 (Wage and Tax Statement) that shows the wages paid and taxes withheld for the year for each employee. To help ensure you're prepared, here is some key information on components of the Form W-2 to help you prevent complications later on.

TABLE OF CONTENTS |

Form W-2 BoxesReported WagesFrequently Asked Questions |

Form W-2 Boxes

Box a - Employee's Social Security Number

-

This is the number that is being used to file your employee's taxes.

Box b - Employer Identification Number (EIN)

-

The Employer Identification Number is assigned to you by the IRS and should be the same number that you use on your federal employment tax returns (e.g., Form 941, Form 944, Form CT-1 or Schedule H, Form 1040).

Box c - Employer's name, address, and ZIP code

-

Box C should contain the employer's legal name, address, and ZIP code. The address should be the same shown on your:

-

Forms 941, 941-SS, 943, 944, CT-1; or

-

Schedule H (Form 1040).

-

Box d - Control Number

-

This is used by ADP to identify your company by your Client Code and Branch Number.

-

For employees: this number can be used to electronically import the W-2 details into tax processing software, to make tax filing easy!

Box e/f - Employee's name, address, and ZIP code

-

This is an employee's first name, middle initial, and last name, exactly as it shows on their Social Security card.

Don't do the following:

-

-

Enter a suffix (for example, Jr. or Sr.) unless it is used on the employee's Social Security card.

-

Include title or academic degrees.

-

Box 1 - Wages, Tips, and Other Compensation

-

The amount of earned income that is taxable for Federal Income Tax only. This amount typically includes regular income, tips, taxable fringe benefits (such a s Group Term Life Insurance etc.) etc. Pre-tax deductions, like qualified medical insurance and retirement contributions will reduce this amount.

-

For a full explanation of the breakdown, refer to the Reported Wages section.

Box 2 - Federal Income Tax Withheld

-

This is the total amount of federal income tax that was withheld from your employee's wages, and would include any additional federal income taxes collected for supplemental wages, additional tax overrides, fringe benefits, etc.

Box 3 - Social Security Wages

-

The amount of earned income that is taxable for Social Security, up to the current limit on wages ($176,100 for 2025). The amount typically includes regular income, taxable fringe benefits (Such as Group Term Life Insurance etc.), etc. Pre-tax deductions, like qualified medical insurance and retirement contributions will reduce this amount.

-

For a full explanation of the breakdown, refer to the Reported Wages section.

Box 4 - Social Security Tax Withheld

-

This is the total amount of Social Security tax that was withheld from your employee's wages. Employer-paid Social Security taxes are not reflected in this amount.

Box 5 - Medicare Wages and Tips

-

The amount of earned income that is taxable for Medicare tax only and typically includes regular income, tips, taxable fringe benefits (such as Group Term Life Insurance, etc.), etc. Pre-tax deductions, like qualified medical insurance, will reduce this amount. For a full explanation of the breakdown, refer to the Reported Wages section.

Box 6 - Medicare Tax Withheld

-

This is the total amount of Medicare tax that was withheld from your employee's wages. Employer-paid Medicare taxes are not reflected on this amount.

Box 7 - Social Security Tips

-

The amount of tips that your employee reported during the calendar year. This amount is only for Social Security taxation purposes. For all other taxes, tips are included in the appropriate wages box (i.e., Box 1, Box 5, Box 16, etc.).

Box 8 - Allocated Tips

-

For large food and beverage establishments, allocated tips may be required if your employee's reported tips are less than 8% of their food and beverage sales (gross receipts). This shortfall amount is reported to the IRS for taxing purposes.

Box 9 - No Longer Used

-

This grayed out box was formerly used for reporting advance payments for the Earned Income Credit tax perk, which ended in 2010.

Box 10 - Dependent Care Benefits

-

This amount includes the total dependent care benefits that your employer paid to you or incurred on your behalf. This includes amounts from a section 125 (cafeteria) plan. Any amount over your employer's plan limit is also included in Box 1. See Form 2441.

Box 11 - Nonqualified plans

-

Nonqualified plans are:

-

A type of retirement plan that does not meet the IRS requirements to be tax sheltered.

-

Designed to benefit executives and key employees.

-

Generally taxable (they typically also appear in Box 1).

-

Note: 401(k) plans, SIMPLE Plans, and 403(b) plans are considered qualified retirement plans and are not listed in this box.

Box 12 - 12a, 12b, 12c, 12d - See instructions for Box 12

-

Box 12 reports a variety of specific earnings or deductions to the IRS.

-

The code indicates the type and the dollar amount associated with it will be listed to the right.

-

Common codes include:

-

C- Group Term Life Insurance Taxable Premiums

-

D- 401(k) employee contributions

-

W- Employer contributions to Health Savings Accounts (HSAs)

-

AA - Roth 401(k) employee contributions

-

For the full list of codes and descriptions, refer to the IRS' detailed instructions for the W-2.

Box 13 - Stat Emp, Ret plan, 3rd party sick pay

Statutory Employee (Stat Emp)

This is a specific type of worker (such as food or beverage drivers, full-time life insurance agents, sales associates in food and lodging industries, etc.) whose wages are taxed differently than regular earnings. See IRS Publication 15-A for more information on these workers.

Retirement Plan (Ret Plan)

If your employee is actively participating in a qualified retirement plan, like a 401(k), SIMPLE or pension plan, this box should be checked.

3rd Party Sick pay

This box is checked if your employee received disability payments paid out through a 3rd party, like a state disability fund, Aflac, etc. A separate W-2 will be included for the disability amounts.

Box 14 - Other

-

This box is used for informational purposes.

-

If your business is located in certain states, employee-paid state unemployment, disability and/or family medical leave taxes will be listed.

- Some earnings and deductions will automatically print out in Box 14, such as personal use of a company car or housing.

Box 15 - State/ Employer's State ID no.

-

This lists the postal abbreviation for your employee's work location.

-

The state-issued identification number will be listed to the right, as required by state regulation.

Box 16 - State wages, tips, etc.

-

This is the amount of earned income that is taxable for State Income tax only.

-

The amount typically includes regular income, tips, taxable fringe benefits (such as Group Term Life Insurance, etc.), etc. Pre-tax deductions, such as qualified Medical insurance and retirement contributions may reduce this amount based on state tax regulations. For a full explanation of the breakdown, refer to the Reported Wages section.

Box 17 - State Income Tax

-

This is the total amount of State Income tax that was withheld form your employee's wages.

Box 18 - Local wages, tips, etc.

-

This is the amount of earned income that is taxable for Local income tax only (if appropriate).

-

The amount typically includes regular income, tips, and taxable fringe benefits (Such as Group Term Life Insurance, etc.), etc. Pre-tax deductions, like qualified Medical insurance and retirement contributions may reduce this amount, based on local tax regulations. For a full explanation of the breakdown, refer to the Reported Wages section.

Box 19 - Local Income Tax

-

This is the total amount of Local Income tax that was withheld from your employee's wages.

Box 20 - Locality Name

-

If your employee has local wages and pays local taxes, an abbreviation of their local jurisdiction (township, city, etc.) will be shown.

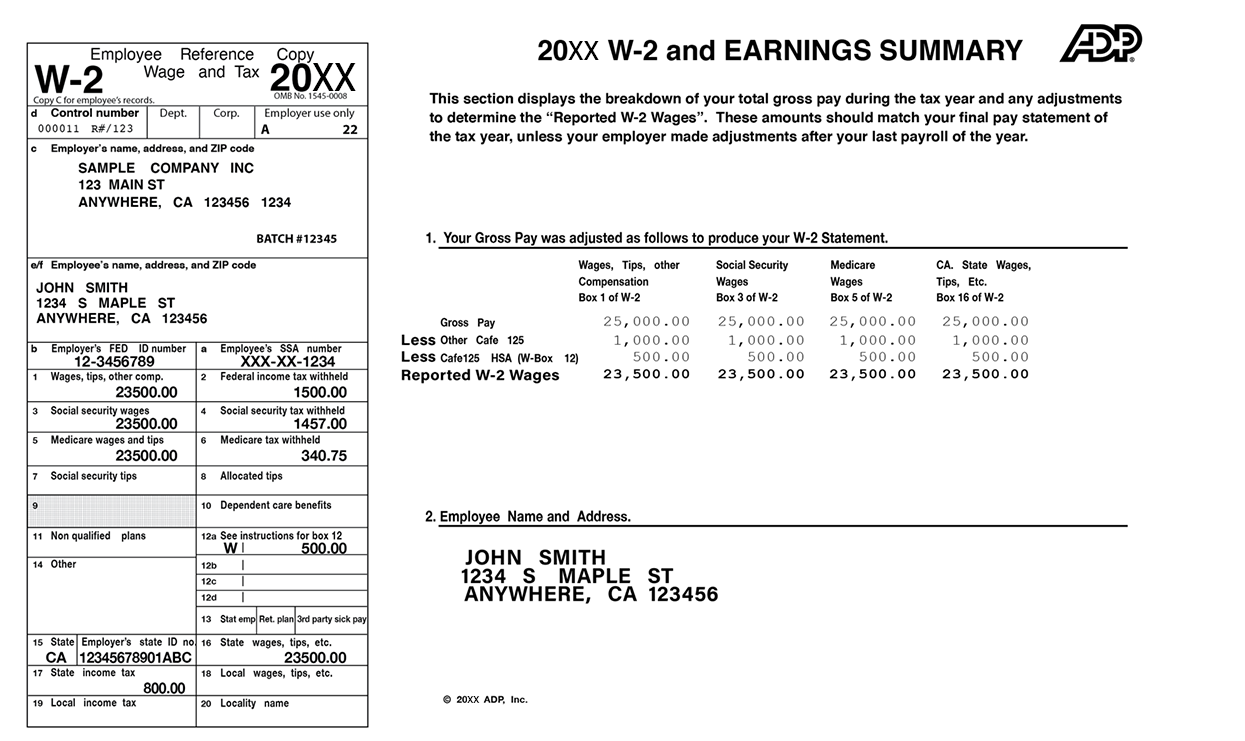

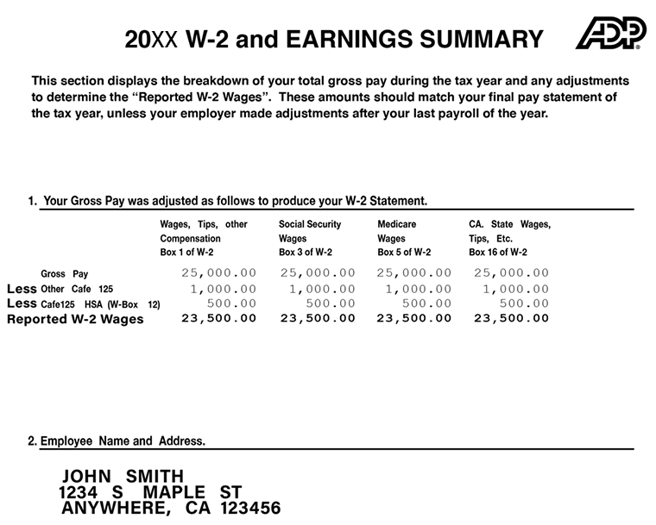

Reported wages

This breakdown shows what earnings or deductions affected the Gross Pay earnings. It also identifies how the taxable wage amounts were calculated for Box 1, Box 3, Box 5, Box 16, and Box 18.

Frequently asked questions

Q: What is gross pay?

A: Gross pay is the amount your employees earn before taxes, benefits and other payroll deductions are withheld from their pay.

Q: What are taxable wages?

A: Taxable wages are the amounts of Gross Pay that is taxed, and can be increased by paying additional earnings or offering fringe benefits or reduced by contributions to pre-tax deductions like 401(k), qualified health insurance, and other cafeteria plan deductions.

Various earnings and deductions may be treated differently for each federal, state, or local tax. To understand how taxable wages were calculated on this form, refer to the Reported Wages section.

Q: When do I have to give Form W-2 to my employees?

A: Under Social Security Administration guidelines, the W-2s are due to your employees on or before January 31 of each year. However, if the due date for filing a return falls on a Saturday, Sunday, or legal holiday, then you may file the return on the next business day.

So, for 2025 W-2s, they are due to your employees on or before February 2, 2026 this year. If you are mailing the forms, they must be postmarked on or before February 2, 2026. Failing to provide W-2s to employees or providing them late can subject a business to added penalties from the various tax agencies.

Q: Why are Box 1, Box 3, and Box 5, different?

A: Each of these boxes reports the wages that are taxable for their respective taxes. Various earnings and deductions may affect one or more of these boxes, based on IRS regulations.

Example: Employee contributions to qualified retirement plans, like a 401(k), will reduce Box 1, but will not affect Box 3 and Box 5.

To see how the taxable wages were calculated, refer to the Reported Wages section.

Conclusion

Make sure you understand and are complying with your Form W-2 responsibilities. You can find more information in the IRS General Instructions for Forms W-2 and W-3. The IRS website also has great information about the W-2.

Share on social